The RIBA Plan of Work is the UK construction sector’s most widely recognised framework, providing a common set of stages used by architects, engineers, cost consultants, contractors and owners. Within the broader UK Construction Lifecycle, it offers a consistent reference point for coordinating design development, procurement and construction activity. Its 2020 update strengthened requirements around sustainability and post-occupancy evaluation in response to the UK’s net-zero commitments, but its primary function remains.

While the RIBA stages are effective for managing design progression, construction projects are rarely managed financially using the same structure. In practice, real estate developers, asset owners, quantity surveyors, fund monitors and project controls teams manage cost through a seven-stage financial lifecycle.

This financial lifecycle reflects how construction budgets change, how risks shift, and how cost certainty develops as design, procurement and delivery information matures, driven by the risk dynamics:

- Early feasibility carries high uncertainty and broad contingencies

- Design development introduces scope evolution and technical risk

- Procurement exposes assumptions to live market pricing

- Construction brings programme risk, contractual variations (JCT), compensation events (NEC), preliminaries drift and supply-chain pressure

- Handover and the defects liability period introduce additional financial responsibilities often underestimated in early planning

Even with structured frameworks, cost overruns remain common due to fragmented cost data, disconnected site information and the complexity of managing cost documentation across all involved stakeholders. Effective financial governance depends on anticipating how costs and risks move through the lifecycle: controlling contingency, maintaining accurate cost-to-complete forecasts, and administering contractual change consistently through variations, extensions of time and compensation events.

This article examines how costs, risks and contingencies shift across each stage of a UK construction lifecycle, and showcases how stage-based financial control can help maintain forecast accuracy and commercial discipline.

Read also: Construction Cost Management Trends in 2026: Market Reset and the Commercial Control Loop

Table of Contents

1. Construction in the UK: How the Financial Lifecycle Operates in Practice

Financial control in construction depends on how information develops over time. UK project teams structure cost management around stages that align with design maturity, procurement activity and contractual responsibility, rather than design stages alone.

This stage-based cost control approach creates a clear financial lifecycle, allowing budgets, risks, contingencies and work packages to evolve in a controlled manner as the project progresses. While terminology varies between organisations, the lifecycle typically includes the following stages:

- Strategic Definition

- Concept & Feasibility

- Design Development

- Pre-Construction & Procurement

- Construction & Delivery

- Handover & Commissioning

- Closing & Post-Completion

Each stage corresponds to a distinct shift in cost certainty, commercial exposure, supply-chain engagement and risk ownership. As construction projects progress:

- Cost plans evolve from high-level estimates to detailed work-package pricing

- Risks move from strategic allowances to defined contractual exposures

- Contingency transitions from broad buffers to specific residual risk cover

- Work packages get procured in line with design maturity

- Contracts get administered under JCT or NEC

- Lenders release funds through staged drawdowns informed by cost-to-complete forecasts and progress verification

How costs are managed at each stage directly affects forecast accuracy, contingency discipline and final account outcomes. Therefore, understanding how cost drivers change across the construction lifecycle is fundamental to preventing cost overrun before it materialises.

2. The Financial Stages of UK Construction Lifecycle

Stage 1 — Strategic Definition: Project Intent and Early Risk Positioning

Strategic Definition establishes the commercial foundation of the construction project by clarifying the owner’s objectives, constraints and performance requirements before feasibility or design work begins.

At this stage, the team identifies site constraints, planning context, regulatory requirements, programme drivers and sustainability objectives, including any net-zero commitments that will influence scope and specification. The purpose is to determine whether the proposed development is strategically viable and what conditions must be satisfied before progressing.

Cost information at this stage is highly indicative. Early estimates are based on benchmark data and high-level assumptions regarding building type, scale and complexity. Because uncertainty is at its highest, risk identification focuses on strategic exposures such as planning risk, ground conditions, access constraints, utilities capacity and regulatory compliance.

Contingency at this stage functions as a strategic allowance rather than a quantified risk provision, reflecting unknowns that cannot yet be defined or measured.

The outputs of Strategic Definition inform the project brief, frame early commercial boundaries and establish the initial risk position that guides the scope of feasibility work in Stage 2.

Stage 2 — Concept & Feasibility: Development Appraisal, CAPEX Definition and Strategic Contingency

During Concept & Feasibility, the owner’s team develops the project appraisal, defines Capital Expenditure (CAPEX) parameters and tests viability against planning policy, site conditions and regulatory constraints.

The appraisal sets out the anticipated CAPEX profile, funding assumptions, programme strategy and initial risk allowances. This stage determines whether the project is financially viable, technically deliverable and aligned with the owner’s risk appetite.

Cost estimates remain high-level and are derived from benchmark rates adjusted for site context, early design principles and assumed construction methodology. Design information is limited, so commercial certainty remains low.

Contingency at this stage is a owner-side strategic buffer, typically higher than at later stages, reflecting planning risk, ground uncertainty, scope development risk and market volatility. It is not tied to specific packages but held to absorb unknowns inherent in early decision-making.

A preliminary risk register is established to capture key uncertainties that will later be refined and, where appropriate, quantified. The outputs of Concept & Feasibility define the CAPEX envelope within which design development must proceed.

Although estimates at this stage are approximate, the discipline applied to documenting assumptions and risk allowances directly affects downstream construction cost control and forecast reliability.

Stage 3 — Design Development: Construction Cost Planning, Quantification and Structure

As the project enters Design Development, cost certainty improves as design information becomes measurable. The quantity surveyor plays a central role in translating design intent into quantified scope and aligning cost assumptions with developing technical solutions.

Design decisions now carry direct cost implications. Changes to structure, M&E strategy, façade systems or spatial layout can materially affect the project’s cost profile.

A key output of this stage is the cost breakdown structure (CBS), which organises the project into logical, traceable cost components. The CBS underpins cost planning, procurement, reporting and later contract administration.

Cost plans are iteratively developed as design matures, typically progressing through Cost Plans A, B and C. As assumptions are replaced by quantified scope, uncertainty reduces and elements of strategic contingency are reallocated or released.

Core activities include elemental cost planning, quantity take-offs, work-package definition, preliminaries development and preparation of the Bill of Quantities (BoQ) where required. The BoQ forms the quantified basis for tender pricing and directly affects provisional sums, tender comparability and downstream commercial risk.

Design risk remains a key exposure at this stage. Incomplete or unresolved design can necessitate provisional sums and create misalignment between the Employer’s Requirements, BoQ and pricing documents. Close coordination between the design team and commercial team is essential to preventing scope ambiguity entering procurement.

Read more: Cost Uncertainty in Construction: The Impact on Quantity Surveying and Financial Control

Stage 4 — Pre-Construction & Procurement: Market Testing and Risk Allocation

During Pre-Construction & Procurement, the commercial focus shifts from estimating to establishing the contractual cost baseline.

Design-stage cost plans are tested against live market pricing through tendering. Tender documentation comprises the technical design, specifications, BoQ or activity schedules, pricing documents and contract conditions.

Tender returns are assessed not only on price but on assumptions, exclusions, programme commitments and risk allocation. This process confirms whether pricing reflects a consistent interpretation of scope and a realistic market position.

Procurement is also where contractual risk is formally allocated:

- Under JCT Design & Build, alignment between the Contractor’s Proposals and the Employer’s Requirements is critical

- Under NEC, the accuracy of the Scope, Activity Schedule and programme is central to cost and risk control

Market testing often exposes gaps between construction cost-plan assumptions and supply-chain pricing due to inflation, capacity constraints, long-lead items or residual design uncertainty. Reconciliation may require use of contingency to absorb justified variances or to retain provisional allowances.

Effective procurement establishes a defensible cost baseline, reducing the likelihood of disputes and uncontrolled change during construction.

Stage 5 — Construction & Delivery: Cost Control and Contract Administration

Once construction begins, previously identified risks convert into live cost and programme exposure. Commercial control now depends on monitoring progress, commitments, change events and contractual compliance.

Supply-chain performance is a major risk driver. Labour availability, material lead times, sequencing dependencies and subcontractor solvency all affect programme and cost outcomes. Re-measurable packages and complex M&E interfaces are particularly exposed.

Construction cost control relies on validating progress against programme, assessing contractor applications for payment, monitoring preliminaries expenditure and administering change under the contract:

- Under JCT, this includes variations, extensions of time and loss-and-expense

- Under NEC, it involves early warnings, compensation events and programme acceptance

Accurate records are essential. Poor documentation or delayed administration often leads to inflated final account positions and unresolved claims.

As changes arise, contingency may be drawn down where costs exceed remaining allowances or where contractual mechanisms transfer risk to the owner. Maintaining an accurate cost-to-complete forecast is critical to identifying emerging exposure and preventing cumulative overrun.

Stage 6 — Handover & Commissioning: Completion and Residual Cost Risk

As the project approaches completion, commercial focus shifts from production to verification. Although construction activity reduces, cost exposure remains significant.

Practical Completion cannot be achieved until commissioning is complete, statutory approvals are secured and contractual documentation — like O&M manuals, as-built information and certification — is provided. Delays in these activities can extend preliminaries and increase cost exposure.

On top of that, snagging and defect resolution require coordinated subcontractor attendance and can create programme pressure if responsibilities are unclear or issues are identified late.

Following Practical Completion, the project enters the Defects Liability Period. While construction has ceased, residual risk remains in relation to latent defects, system performance and retention release. Effective control at this stage depends on accurate valuation, disciplined use of remaining contingency and structured close-out procedures.

Stage 7 — Construction Closeout & Post-Completion: Final Account and Retention

After Practical Completion, the commercial focus shifts to final account agreement and construction contractual close-out.

Outstanding variations, provisional sums, measured works and claims are reviewed against contractual entitlement. Accurate records from earlier stages are essential to resolving valuation efficiently and avoiding prolonged disputes.

During the Defects Liability Period, the contractor’s response to defect notifications affects retention release and final account timing. Poor defect management frequently delays financial close-out.

Moreover, effective closeout requires coordinated input from the QS, contract administrator, project manager and owner’s team to confirm that all obligations have been met and the project can be closed both contractually and financially.

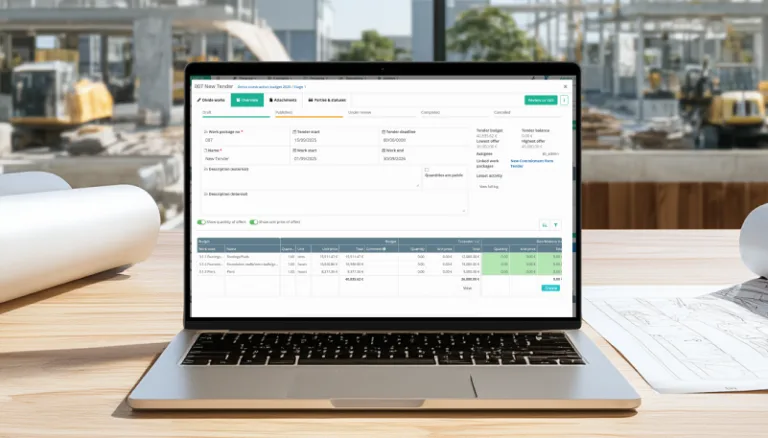

3. How Bauwise Subprojects Support Stage-Based Cost Control

Across the construction lifecycle, budgets, risks and contingencies do not remain static. They change as design matures, procurement reveals market pricing and construction exposes site conditions and coordination issues.

Traditional spreadsheet-based workflows struggle to reflect these shifts, particularly where stage-specific budgets, contingency use, work-package commitments and contract-specific costs must be tracked separately.

Bauwise’s subproject structure allows projects to be managed by financial stages, with each stage operating as its own cost control unit — holding its own budget, forecast, contingency, risks, work packages, commitments and actuals — while still rolling up into a consolidated project view.

This reflects how cost control is organised in practice by real estate developers, QS teams and monitoring surveyors. Stage-level segregation maintains transparency over contingency use, prevents later-stage construction costs from distorting earlier budgets, and supports lender drawdowns and cost-to-complete reviews.

Bauwise subprojects support:

- Stage-specific contingency tracking

- Forecast-to-complete aligned with work-package progress

- Package-level cost control under JCT and NEC

- Stage-based reporting for fund monitoring

- Clear segregation of risk and scope exposure

- Optional phasing or plot-based structuring on multi-phase developments

Rather than introducing a new methodology, the structure reflects established commercial practice and supports disciplined cost control aligned with real construction project lifecycles.

Conclusion — How to Effectively Manage Costs Across the UK Construction Lifecycle

Cost overruns in UK construction are rarely the result of a single failure. They emerge when financial control does not evolve in line with how information, risk and contractual exposure change across the project lifecycle. While design may follow the RIBA Plan of Work, effective cost management operates through a financial lifecycle in which uncertainty reduces, risk becomes defined and cost certainty is progressively tested against market pricing and site conditions. Managing contingency, forecasts and change consistently at each stage is essential to maintaining a defensible cost baseline and achieving predictable final account outcomes.

Stage-based financial control provides the structure needed to align budgets, risks and commercial decisions with the realities of design development, procurement and construction. By separating cost management by stage while maintaining a consolidated project view, teams can track contingency use, control work-package exposure and maintain accurate cost-to-complete forecasts. This approach reflects established UK commercial practice and remains fundamental to disciplined cost governance, lender confidence and effective contract administration through to construction closeout.

Read also: How Synced ERP and Accounting Software Data Can Unlock Real-Time Construction Cost Control

About the Author

Mikk Ilumaa

Mikk Ilumaa is the CEO of Bauwise, a leader in construction financial management software with over ten years of experience in the construction software industry. At the helm of Bauwise, Mikk leverages his extensive background in developing construction management solutions to drive innovation and efficiency. His commitment to enhancing the construction process through technology makes him a pivotal figure in the industry, guiding Bauwise toward setting new standards in construction financial management. View profile